Prefab Home Financing Ontario: Construction Mortgages, CMHC & How to Get Approved

Prefab homes in Ontario are financed through construction mortgages with staged draw schedules — not standard purchase mortgages — when the home is under construction.

Once built and permanently affixed to a permanent foundation, CSA A277 certified factory-built homes qualify for standard residential mortgages including CMHC insurance with as little as 5% down.

Understanding which financing structure applies to your specific build situation before approaching any financial institutions is the most important first step in any Ontario prefab home purchase.

No obligation. Construction mortgage ready — we provide the complete lender documentation package for your Ontario build.

Why Prefab Home Financing Works Differently Than Traditional Homes

Most Ontario buyers approaching prefab home financing for the first time arrive with one of two assumptions — either that prefab homes cannot be financed like regular homes, or that they can be financed exactly like traditional builds.

Both assumptions are partially wrong, and both lead to the same outcome: buyers who approach lenders without understanding which financing structure applies to their situation waste weeks in the approval process and sometimes lose building seasons entirely.

The financing structure for a prefab home in Ontario is determined by two variables that have nothing to do with the model you select or the builder you choose.

The first is whether your home is already built and installed or still under construction. The second is whether the land the home sits on is owned land or leased land.

These two variables determine everything about your lender options, your down payment requirements, your interest structure during the build period, and your Canada Mortgage and Housing Corporation insurance eligibility.

For a complete overview of prefab home types, prices, and models available across Ontario see our Prefab Homes Ontario guide.

The Core Distinction — Under Construction vs Already Built

Two fundamentally different financing situations apply to Ontario prefab home buyers.

Understanding them before you approach any lender is what separates buyers who get approved quickly from those who lose weeks to documentation gaps and misdirected applications.

Prefab home financing in Ontario is determined by two variables before any lender is contacted — whether the home is under construction or already built, and whether the land is owned or leased.

Not sure which financing path applies to your build? We’ll walk you through your options based on your land, budget, and timeline — so you can move forward with confidence.

If your home is under construction or not yet installed on a permanent foundation you need a construction mortgage — a staged-draw product that releases funds at verified build milestones rather than in a lump sum at purchase.

If your home is already built and permanently affixed to a foundation meeting Ontario Building Code and CSA A277 standards it qualifies for a standard residential mortgage through the same lenders and at comparable rates to site-built homes.

This distinction determines your entire financing pathway.

A buyer who approaches big banks for a standard mortgage on a home not yet built will be redirected to the construction mortgage team.

A buyer who approaches for a construction loan on a home already installed on a permanent foundation will be redirected to the standard residential mortgage team.

Understanding which situation applies before making any lender contact saves two to four weeks of process time on a build where every week matters for seasonal scheduling in Ontario.

What Lenders Actually Evaluate on a Prefab Mortgage Application

Lenders evaluate six specific factors on Ontario prefab home financing applications that they do not evaluate on standard residential purchase mortgages.

First, CSA A277 certification — the Canadian Standards Association standard that qualifies factory-built homes for mortgage financing and CMHC insurance and distinguishes permanently affixed prefab homes from mobile homes and manufactured structures.

Second, Ontario Building Code compliance for the specific model and construction system.

Third, permanent foundation affixation covering foundation type, geological suitability for the building site, and permanence of installation.

Fourth, land ownership status — owned land versus leased land determines the entire financing structure.

Fifth, builder credentials and documentation quality including lender-ready engineering drawings, cost breakdowns, and construction timelines.

Sixth, appraisal as-completed value — lenders require confirmation before releasing funds that the finished home will reach the appraised value assumed in the financing approval.

My Own Cottage provides complete lender-ready documentation packages for every Ontario build — CSA certification records, stamped engineering drawings, construction timelines, milestone completion reports, and detailed cost breakdowns.

Every package is formatted to meet the submission requirements of major banks, non-bank lenders, and credit unions before you approach any lender.

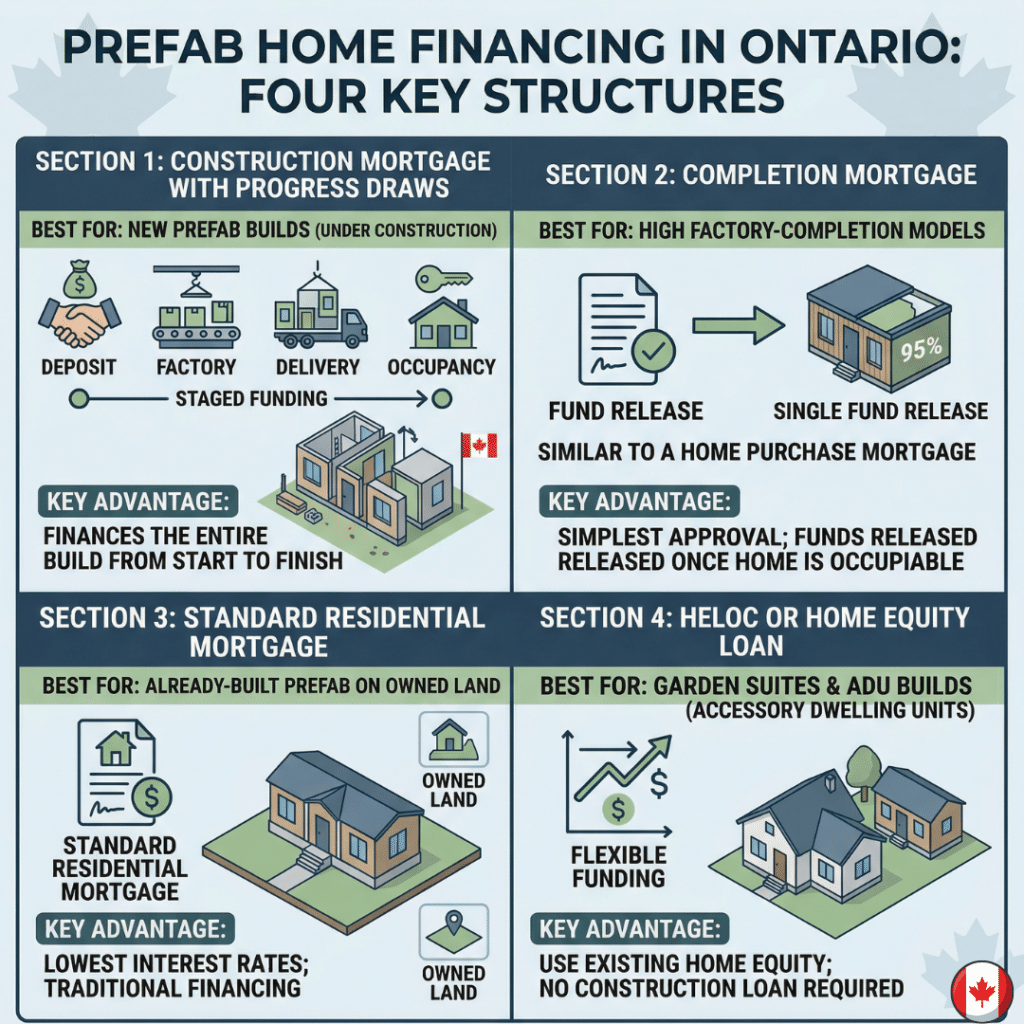

The Four Financing Structures for Ontario Prefab Home Buyers

The four financing structures below represent fundamentally different products serving fundamentally different buyer situations — the structure that applies to your build is determined before you select a model, not after.

Understanding which of the four structures applies to your situation before approaching any lender saves two to four weeks in the approval process.

Now that you understand the four financing structures, the next step is to see what your build actually looks like — based on your budget, land, and goals.

| Financing Type | Best For | Key Advantage |

|---|---|---|

| Construction Mortgage with Progress Draws | New prefab builds under construction | Funds align with build milestones |

| Completion Mortgage | High factory-completion models | Fastest approval, single release |

| Standard Residential Mortgage | Already-built prefab on owned land | Full lender competition, best rates |

| HELOC or Home Equity Loan | Garden suites and ADU builds | Flexible draws, no draw inspections |

Construction Mortgage with Progress Draws — The Most Common Structure

The construction mortgage with staged progress draws is the standard financing structure for Ontario buyers building a new prefab home.

Funds are released at verified construction milestones — typically deposit, factory build completion, delivery and installation, and final occupancy — rather than as a lump sum at the land purchase stage.

Interest is charged only on the funds released at each stage, not on the full loan amount.

This staged interest structure meaningfully reduces total financing costs during the build period compared to carrying the full mortgage amount from day one.

On a $300,000 construction loan at 7% annual interest, paying interest only on staged draws rather than the full amount from day one saves approximately $8,000 to $15,000 over a four to eight month prefab build period.

This financing advantage compounds further when compared to traditional home construction, which routinely carries construction loan interest for twelve to eighteen months — meaning prefab buyers save on both the staged draw structure and the shorter total timeline simultaneously.

Lenders require progress draw inspections at each milestone confirming the build has reached the claimed stage before releasing the next fund tranche.

Construction mortgage rates in Ontario typically run 0.50% to 1.25% above standard residential mortgage rates due to the staged draw structure and higher lender oversight requirements.

Once construction is complete and the home passes final inspection the construction mortgage converts to a standard residential mortgage at current term rates — a process called mortgage conversion that My Own Cottage coordinates with lenders to ensure smooth and timely transition.

See what your budget actually builds — explore prefab home designs designed for Ontario lots, financing structures, and real-world project costs.

Completion Mortgage — For High Factory-Completion Prefab Models

A completion mortgage releases the full mortgage amount in a single transaction once the prefab home is installed, inspected, and certified as complete — rather than in staged draws during the home construction process.

This structure is available for prefab models with high factory completion percentages where the majority of home-building work happens in the controlled environment of the factory before delivery rather than on site.

Completion mortgages are simpler and faster to administer than progress-draw mortgages and are increasingly available for CSA A277 certified modular builds delivered nearly complete to the building site.

The qualification requirements mirror a standard residential mortgage — permanent foundation, CSA certification, Ontario Building Code compliance, and standard borrower qualification criteria.

My Own Cottage can advise which models in the catalogue qualify for completion mortgage financing based on their factory completion percentage at the time of model selection.

Standard Residential Mortgage — For Already-Built Prefab Homes

If you are purchasing a CSA A277 certified prefab home already permanently affixed to a foundation and meeting Ontario Building Code standards, standard residential mortgage financing applies through the same lenders and at the same rate structures as comparable site-built homes.

This includes existing modular homes on lots you are purchasing — any permanently affixed certified prefab home that is already built and installed is treated by lenders as equivalent to a site-built home for financing purposes.

The home is appraised using standard residential comparable sales methodology.

The land secures the loan.

The construction method is irrelevant to lender risk assessment as long as CSA standards and permanent foundation affixation are confirmed.

This financing equivalency is precisely what gives modular and CSA A277 certified panelized prefab homes their resale value comparability to traditional homes — the real estate financing market treats them the same when the certification and foundation criteria are met.

This is the financing outcome that converts a factory-built home into real property for tax, valuation, and financing purposes.

HELOC and Home Equity Loans — For Garden Suite and ADU Builds

For Ontario homeowners adding a garden suite, laneway home, or accessory dwelling unit to an existing property, home equity loans and Home Equity Lines of Credit are increasingly common and often lower-cost alternatives to a new construction mortgage.

The existing property secures the line of credit. Funds are drawn as needed during the build rather than released in lender-supervised milestone draws — eliminating draw inspection fees and the administrative timeline of staged draw approvals.

HELOC financing is particularly well-suited to garden suite and ADU builds because the rental income generated by the completed secondary dwelling can service the debt independently of the primary household income.

A garden suite generating $1,800 to $2,500 per month in rental income on a typical HELOC balance effectively becomes self-financing over a four to eight year period — making it one of the strongest investment cases available to Ontario property owners in the current housing market.

Ontario’s Bill 23 provisions have reduced or eliminated development charges for qualifying garden suite builds in many municipalities, meaningfully reducing the total project cost that requires financing and improving the rental income to debt service ratio.

→ Affordable Prefab Homes Ontario — garden suite and ADU guide

CMHC Insurance and Default Mortgage Insurance for Prefab Homes in Ontario

Which Prefab Home Types Qualify for CMHC Insurance

Canada Mortgage and Housing Corporation mortgage insurance — the default mortgage insurance that enables buyers to purchase with less than 20% down — is available for Ontario prefab home builds that meet four specific qualification criteria simultaneously.

CMHC insurance is available when all four criteria are met — enabling eligible buyers to purchase with as little as 5% down.

• The home must be permanently affixed to a permanent foundation

• The factory construction must be CSA A277 certified

• The completed home must meet Ontario Building Code requirements

• The home must be used as the buyer’s owner-occupied primary residence on owned land — not leased land and not a seasonal or recreational structure

When all four conditions are met CMHC insurance allows eligible Ontario prefab home buyers to purchase with as little as 5% down — the same minimum down payment that applies to conventional site-built home purchases.

CSA A277 certified modular builds on permanent foundations consistently meet CMHC eligibility criteria.

CSA A277 certified panelized prefab homes on permanent foundations also qualify.

Manufactured homes on leased land such as mobile home parks do not qualify for CMHC insurance — they require a chattel mortgage rather than a residential mortgage as explained in the next section.

Canada Guaranty and Sagen are alternative providers of default mortgage insurance in Canada and apply similar eligibility criteria to CMHC for factory-built homes on owned land with CSA certification.

CMHC Insurance Premiums — What Ontario Prefab Buyers Actually Pay

CMHC insurance premiums for qualifying prefab home purchases follow the same premium schedule as conventional home purchases.

A purchase with 5% to 9.99% down carries a premium of 4.00% of the insured loan amount.

A purchase with 10% to 14.99% down carries a premium of 3.10%. A purchase with 15% to 19.99% down carries a premium of 2.80%.

Premiums can be added to the mortgage amount and amortized over the full mortgage term rather than paid as an upfront extra cost at closing.

For a qualifying prefab home with a total project cost of $300,000 and a 5% down payment of $15,000 the insured loan amount is $285,000 and the CMHC premium is $11,400 — which can be added to the mortgage producing a total insured mortgage of $296,400.

This is the financing structure that makes new prefab home ownership accessible for first-time buyers and first-time homebuyer households without the 20% down payment that uninsured purchases require.

→ External link: CMHC mortgage insurance

Traditional Mortgage vs Chattel Mortgage — The Land Ownership Question

The land ownership question below determines your entire financing pathway — the same prefab home on owned land and leased land produces two fundamentally different financing outcomes with meaningfully different long-term financial implications.

Land ownership determines your financing — owned land qualifies for traditional mortgages, while leased land requires higher-cost chattel financing.

Traditional Mortgage — For Prefab Homes on Owned Land

A traditional mortgage is available for CSA A277 certified prefab homes permanently affixed to owned land — land registered in your name with a standard real property title.

• The land secures the loan

• The home is classified as real property

• Standard residential amortization applies — up to 25 years for insured mortgages and up to 30 years for uninsured mortgages

All major Canadian big banks, non-bank mortgage lenders, and credit unions offer traditional residential mortgages for qualifying prefab homes on owned land meeting CSA standards.

This is the financing structure that gives permanently affixed prefab and modular builds their full residential mortgage eligibility, their property tax classification as real estate, and their resale value comparability to site-built homes.

The loan terms, features, and approval process for a traditional mortgage on a CSA A277 certified prefab home on owned land are functionally equivalent to a traditional mortgage on a site-built home — the same lenders, the same rates, the same amortization options.

Payment requirements including standard principal and interest payments, property taxes, and home warranty coverage apply in the same way as for any Ontario residential mortgage.

Chattel Mortgage — For Prefab Homes on Leased Land

A chattel mortgage applies when a prefab home is placed on leased land — for example in a mobile home park or modular home community where you pay a lease agreement for the land rather than owning it.

The home is treated as personal property rather than real estate — similar to the way an auto loan treats a vehicle. Because there is no land title to secure the loan the home itself is the collateral.

Loan terms are shorter — typically 15 to 20 year maximum amortization — and interest rates are higher than traditional mortgage rates because the lender cannot use the land as collateral and the home depreciates as personal property rather than appreciating as real estate.

Chattel mortgages are not standard retail mortgage products.

They are available through some big banks via specialized programs, certain credit unions, and alternative or private lenders. CMHC insurance does not apply to chattel mortgages.

The approval process for a chattel mortgage is more restrictive than a traditional mortgage and typically requires the home to be CSA certified, under a specific age limit — often under 20 to 25 years at loan maturity — and located in a recognized lender-approved community.

For Ontario prefab home buyers the practical guidance is straightforward — wherever possible purchase on owned land rather than leased land.

The financing options, the loan terms, the property tax treatment, the resale dynamics, and the long-term value trajectory are all meaningfully better for prefab homes on real property versus personal property on leased land.

Traditional Mortgage vs Chattel Mortgage — Quick Comparison:

| Factor | Traditional Mortgage | Chattel Mortgage |

|---|---|---|

| Land requirement | Owned land | Leased land |

| Security | Land and home | Home only |

| Classification | Real property | Personal property |

| CMHC insurance | Available | Not available |

| Amortization | Up to 25–30 years | Typically 15–20 years |

| Interest rates | Standard residential rates | Higher than traditional mortgage |

| Resale | Standard real estate transaction | Personal property sale |

| Best for | Permanent primary residences | Mobile home park situations |

HST Rebate and GST Relief — The Financing Tools Most Ontario Buyers Miss

No published Ontario prefab home financing guide addresses the HST rebate and GST relief programs as active financing tools — despite the fact that they directly reduce the loan amount required and the CMHC insurance premium calculated on that amount.

On a qualifying project in the $200,000 to $350,000 total cost range these programs can represent a $15,000 to $25,000 reduction in total project cost before a single mortgage payment is made.

Ontario New Home HST Rebate

The Ontario new home HST rebate returns a portion of the provincial 8% HST component on qualifying new home purchases used as primary residences.

For a qualifying prefab home project in the $200,000 to $350,000 total cost range this represents $8,000 to $15,000 in recovered tax.

The rebate phases out at higher purchase prices.

It applies equally to new prefab and modular builds as to site-built homes when the structure is permanently affixed to a foundation and used as a primary residence on owned land.

The practical financing implication is direct — buyers who structure their purchase correctly with their accountant before signing receive a meaningful reduction in their net project cost.

That lower project cost reduces the loan amount required, which in turn reduces the CMHC insurance premium calculated as a percentage of the insured loan amount.

Federal GST Relief for First-Time Home Buyers

The federal GST relief program removes the 5% federal component on qualifying new home purchases up to $1.5 million for eligible first-time homebuyer households.

On a qualifying prefab home project in the $200,000 to $300,000 total cost range this represents approximately $10,000 to $15,000 in recovered tax.

Permanently affixed prefab homes purchased as primary residences on owned land qualify in the vast majority of cases.

Combined the Ontario HST rebate and federal GST relief can represent a five-figure reduction in total project cost — reducing both the financing required and the CMHC insurance premium.

This is among the most underutilized cost-reduction opportunities available to Ontario first-time buyers and first home purchasers in the prefab housing market.

Confirming eligibility and structuring the purchase correctly with your accountant before signing any purchase agreement is one of the highest-value financing preparation steps available to any Ontario prefab home buyer regardless of build size or location.

→ External link: CRA HST rebate and GST relief programs

Lender Types for Prefab Home Financing in Ontario

Major Canadian Banks

All major Canadian big banks — RBC, TD, Scotiabank, BMO, and CIBC — offer construction mortgages and standard residential mortgages for CSA A277 certified prefab homes on owned land.

Bank mortgage approval for prefab homes follows the same qualification criteria as site-built home mortgages when CSA certification, Ontario Building Code compliance, and permanent foundation documentation are complete and in lender-ready format.

Bank home loans for prefab builds can be slower to approve than non-bank lenders because branch staff see prefab applications infrequently and may require additional review time for documentation that is unfamiliar to general mortgage advisors.

Working with a bank’s new construction or builder mortgage team — rather than a standard residential mortgage advisor — significantly accelerates the approval process for factory-built home applications.

Non-Bank Mortgage Lenders and Mortgage Finance Companies

Non-bank lenders and mortgage finance companies including THINK Financial, First National, and Merix Financial often offer more flexible approval criteria and competitive rates for prefab construction mortgages compared to major banks.

These non-bank lenders understand factory-built homes, modular construction processes, and CSA A277 documentation requirements more consistently than general bank branch mortgage advisors who see prefab applications infrequently.

Credit Unions

Ontario credit unions including Meridian, Alterna, and DUCA provide prefab-friendly financing solutions with more flexible underwriting than major banks — particularly for rural builds in Ontario where local appraisers understand regional housing market nuances.

Credit unions evaluate modular builds under the same risk framework as site-built homes when CSA A277 certification and permanent foundation documentation are confirmed.

For Ontario buyers with non-standard income, lower credit history scores, or complex property situations credit unions are often the most practical first financing option before exploring alternative or private lenders.

Alternative and Private Lenders

Alternative lenders including Home Trust and EQ Bank offer prefab construction mortgages for buyers who do not meet major bank qualification criteria — typically due to self-employment income, lower credit history, or non-standard property characteristics.

Rates are higher than major bank or non-bank lender rates but the approval process is more flexible.

Private lenders offer the most flexible criteria and the highest interest rates — typically used as a short-term bridge financing solution for complex sites or borrowers rebuilding credit history who plan to refinance with a standard lender after construction completion.

Qualification Requirements for Prefab Home Financing in Ontario

Borrower Qualification Criteria

Credit history requirements for construction mortgage approval in Ontario typically start at 640 to 680 for major bank and non-bank lenders and can be lower for credit unions and alternative lenders.

Income stability and documented income are essential — lenders must confirm borrowers can service staged construction draws under stress-tested rates as required by OSFI mortgage underwriting guidelines.

Gross debt service ratio and total debt service ratio must fall within standard lender thresholds.

The mortgage stress test applies to all federally regulated lenders regardless of down payment size — qualifying borrowers at the greater of the mortgage contract rate plus 2% or the current qualifying rate.

Property and Documentation Requirements

Lenders require eight specific documentation items for prefab construction mortgage approval in Ontario:

• Proof of land ownership with registered title

• Zoning confirmation showing that residential construction is permitted on the specific lot

• CSA A277 certification documentation provided by the builder

• Engineering drawings and floor plans stamped by a licensed engineer

• Detailed construction cost breakdown covering all line items from site preparation through occupancy

• Construction timeline with milestone dates aligned to the proposed draw schedule

• Builder credentials and track record documentation

• Site plan showing foundation location, setbacks, and utility access

The building permit is typically required before the first construction draw is released — confirm your municipality’s permit application timeline before committing to a construction start date with your builder.

Having complete documentation in lender-ready format before approaching any lender is the single most effective action any Ontario prefab home buyer can take to accelerate the financing process.

Incomplete documentation is the primary cause of delayed approvals on factory-built home applications at every lender type.

Hidden Costs That Affect Your Financing Requirements

The loan amount required for a prefab home build in Ontario is almost always larger than the kit package price alone — because additional costs that are not included in the advertised package price must also be financed.

• Foundation construction adds $12,000 to $85,000 depending on type and site conditions

• Site preparation and grading adds $8,000 to $60,000 depending on terrain

• Utility connections add $8,000 to $70,000 depending on municipal services versus rural well and septic system requirements

• Building permits and development charges add $5,000 to $75,000 depending on municipality (development charges near Orillia range from $7,308 in Gravenhurst to $49,912 in Ramara Township — see our prefab home costs Orillia guide for the complete municipal breakdown)

• Delivery beyond the builder’s standard service radius adds $5,000 to $35,000 for remote Ontario sites

These hidden costs collectively add $80,000 to $200,000 above the base package price on most Ontario prefab projects.

Buyers who approach lenders with only the kit package price as their project cost will be under-financed when the full additional cost picture becomes clear — a situation that can stall or cancel a build that is already underway.

Ontario-Specific Financing Considerations by Region

GTA and Urban Ontario

Development charges in high-growth GTA municipalities — ranging from $50,000 to $75,000 for a single detached home — meaningfully increase total project costs and therefore loan amounts required compared to equivalent builds in smaller Ontario municipalities.

Ontario’s Bill 23 provisions have reduced or eliminated development charges for qualifying garden suite and ADU builds in many GTA municipalities.

HELOC financing for garden suite builds on existing GTA properties is the most common financing structure for urban Ontario prefab ADU projects — the existing property equity funds the build and the rental income services the debt making these builds genuinely self-financing over time.

Muskoka and Cottage Country

Waterfront and cottage country builds in Muskoka, Haliburton, and the Kawarthas face additional lender scrutiny on site access, foundation suitability on Canadian Shield terrain, and seasonal versus year-round occupancy designation.

Year-round primary residence builds on owned land qualify for standard residential mortgage financing.

Seasonal recreational structures — cottages not meeting four-season habitation and building standards — face more restricted lender acceptance and may require vacation property mortgage products at different loan terms and rate structures.

Central Ontario and Simcoe County

Central Ontario sits between the GTA and Muskoka and is one of the most financing-friendly build environments in Ontario — for one specific reason. The City of Orillia delivers full municipal water and sewer to the property line, eliminating the $25,000–$70,000 rural well and septic variable that every surrounding township build must carry. That single distinction reduces the total project cost — and therefore the loan amount required — by a meaningful margin compared to equivalent builds in Severn Township, Ramara Township, or Muskoka.

Development charges near Orillia range from approximately $7,308 in Gravenhurst (District of Muskoka) to $49,912 in Ramara Township, with the City of Orillia sitting at approximately $30,932 under By-law 2024-113. This spread directly affects the construction mortgage amount required — a buyer on a serviced Orillia urban lot is financing materially less total project cost than a buyer on a Ramara Township waterfront lot with LSRCA permit requirements, LSPP-compliant tertiary septic, and higher development charges.

HELOC financing for garden suite and ADU builds is increasingly common in Orillia, where Bill 23 as-of-right permissions and the development charge exemption for qualifying accessory residential units have meaningfully improved the rental income to debt service ratio on secondary suite projects.

For lot-type cost scenarios, the complete development charge breakdown across all five municipalities, and the all-in financing implications by build type, see our prefab homes in Orillia guide.

Northern Ontario

Northern Ontario builds with longer delivery distances, higher energy efficiency specification requirements, and hydro line extension costs have higher total project costs than equivalent Southern Ontario builds on serviced lots.

Lower land prices in Northern Ontario municipalities partially offset these higher costs.

CMHC insurance eligibility is the same in Northern Ontario as in Southern Ontario for qualifying builds — the geographic location of the building site does not affect CMHC insurance eligibility when the property, builder, and borrower criteria are met.

Tiny homes and compact structures in Northern Ontario face the same financing eligibility criteria as larger models — CSA certification and permanent foundation affixation determine financing eligibility, not structure size.

Rural Ontario

Rural Ontario builds requiring well and septic system installation add $25,000 to $70,000 to total project costs above kit package prices — costs that must be included in the construction mortgage financing or covered through supplementary HELOC or personal loan financing.

Confirming which site preparation costs your construction mortgage includes before finalizing your financing structure prevents cash flow gaps during the build that can delay milestone completion and draw release.

Rural properties also face longer building permit timelines in some Ontario municipalities — confirm permit approval lead times before committing to a construction start date.

Ontario vs Other Canadian Provinces

Ontario buyers occasionally reference British Columbia, Nova Scotia, or Atlantic Canada prefab home pricing and financing when researching options — particularly for manufacturers that operate across multiple provinces.

British Columbia’s housing market follows similar CSA A277 standards but with meaningfully different land costs, development charge structures, and lender risk appetites for factory-built homes that make direct financing comparisons unreliable for Ontario project planning.

Nova Scotia and Atlantic Canada prefab markets operate under different provincial building standards and municipal development charge structures.

Ontario-specific figures and Ontario lender relationships are the only reliable basis for Ontario prefab home financing planning.

The Five-Step Prefab Home Financing Process in Ontario

The five steps below represent the complete financing pathway for a new Ontario prefab home build — from initial pre-approval through final mortgage conversion — with the most common delay point at Step 3 where incomplete builder documentation extends approval timelines by four to eight weeks.

Prefab home financing follows five clear steps — having complete CSA A277 and builder documentation ready before Step 3 can significantly speed up approval.

Step 1 — Get Pre-Approved Before Model Selection

Pre-approval is the most important first step in any Ontario prefab home financing process — and the step most buyers skip because they want to browse floor plans and models first.

Pre-approval tells you exactly how much you can borrow under current stress test rates with your specific income, credit history, and debt ratios.

It also identifies which lenders are appropriate for your situation before you invest time in model selection, site visits, and builder consultations.

My Own Cottage recommends every buyer obtain mortgage pre-approval before their first model consultation.

Pre-approval makes every subsequent conversation more productive and prevents the most expensive mistake in Ontario prefab home planning — selecting a model at the edge of your approved limit without accounting for the foundation, site preparation, and utility costs that complete the total project budget.

Step 2 — Select Your Model and Confirm Your Total Project Cost

Model selection determines construction costs, engineering drawings, required foundation type, and the financing structure the lender will evaluate.

The total project cost — model price plus foundation plus site preparation plus utility connections plus building permits and development charges — is the figure the lender finances, not the kit package price alone.

Confirming your total project cost before finalizing model selection prevents the most common prefab financing gap — selecting a model that appears within your pre-approved limit but whose total project cost including all hidden costs exceeds your qualification threshold.

Step 3 — Submit Complete Lender Documentation

Once your model is confirmed and your total project cost is established submit the complete lender documentation package.

My Own Cottage provides this complete package in lender-ready format covering CSA certification, engineering drawings, floor plan specifications, construction timeline, site plan, and detailed cost breakdown — everything the lender needs in the format they require.

Incomplete documentation is the primary cause of delayed approvals and the primary reason prefab mortgage applications stall at financial institutions that see factory-built home applications infrequently.

Step 4 — Draw Inspections and Construction Milestone Verification

During the construction phase the lender conducts progress draw inspections at each milestone to confirm the build has reached the claimed completion stage before releasing the next fund tranche.

Foundation completion, factory build completion, delivery and installation, and final occupancy are the standard milestone sequence for most Ontario prefab construction mortgages.

My Own Cottage aligns its home construction process with standard Ontario lender draw inspection sequences to minimize delays between milestone completion and fund release.

Step 5 — Mortgage Conversion and Final Occupancy

Once the prefab home is installed, inspected, and certified as complete the construction mortgage converts to a standard residential mortgage at current term rates.

The conversion triggers the standard amortization schedule — typically 25 years for CMHC-insured mortgages — and construction-period interest-only payments on staged draws give way to standard principal and interest payments on the full mortgage amount.

My Own Cottage coordinates the final occupancy documentation package with lenders to ensure smooth and timely mortgage conversion.

My Own Cottage — Financing Support for Ontario Prefab Home Buyers

Every My Own Cottage consultation begins with a complete all-in cost estimate for your specific Ontario property — the total project cost figure your lender needs for accurate construction mortgage sizing — before you commit to any model or sign any agreement.

No surprises. No hidden costs.

Just honest numbers specific to your land, your model, and your timeline before any financing decisions are made.

My Own Cottage provides complete lender-ready documentation packages for every Ontario build — CSA A277 certification records, engineering drawings stamped by a licensed engineer, construction timelines, cost breakdowns, and milestone completion reports that meet major lender submission requirements.

Every home is built in a controlled environment to Ontario Building Code standards and CSA A277 certified factory processes — qualifying for standard mortgage financing, CMHC insurance, and Ontario’s new home warranty through Tarion regardless of model size or price point.

We can connect buyers with Ontario lenders and mortgage brokers experienced in prefab and modular construction financing who understand draw schedules, CSA certification documentation requirements, and the specific approval process for factory-built homes in Ontario’s housing market.

My Own Cottage builds and delivers across Ontario — from urban areas in the GTA and Ottawa to cottage country in Muskoka and Haliburton and rural properties in Northern Ontario including areas around Thunder Bay and beyond.

→ Prefab Homes for Sale Ontario — browse models by size and price | → Prefab Homes Ontario — complete hub

Frequently Asked Questions — Prefab Home Financing Ontario

Can I get a mortgage for a prefab home in Ontario?

Yes — CSA A277 certified prefab homes permanently affixed to a permanent foundation on owned land qualify for the full range of residential mortgage financing available to Ontario homebuyers. This includes standard residential mortgages through major banks, non-bank lenders, and credit unions, construction mortgages with staged draw schedules for homes under construction, and CMHC-insured mortgages with as little as 5% down for qualifying primary residence purchases. The key qualification criteria are CSA A277 certification, Ontario Building Code compliance, permanent foundation affixation, and owned land. Manufactured homes on leased land in mobile home parks face a different financing pathway through chattel mortgages rather than traditional residential mortgages.

What are the interest rates for prefab home mortgages in Ontario?

Interest rates for prefab home mortgages in Ontario depend on the financing structure and the lender type. Standard residential mortgages for already-built CSA A277 certified prefab homes on owned land carry the same interest rates as equivalent site-built home mortgages — no rate premium applies when the home meets OBC standards and is permanently affixed to a foundation. Construction mortgages for prefab homes under construction typically run 0.50% to 1.25% above standard residential mortgage rates due to the staged draw structure and higher lender oversight requirements during the build period. Chattel mortgages for homes on leased land carry the highest rates — meaningfully above standard residential rates — because the lender cannot use land as collateral. Once a construction mortgage converts to a standard residential mortgage at occupancy the rate resets to current term rates through the full lender market. Working with a mortgage broker experienced in prefab and modular construction financing — rather than a standard residential mortgage advisor — consistently produces more competitive rate outcomes for factory-built home applications.

What is a construction mortgage and how does it work for prefab homes in Ontario?

A construction mortgage for a prefab home in Ontario releases funds in staged draws aligned with verified build milestones — typically deposit, factory build completion, delivery and installation, and final occupancy — rather than as a lump sum at purchase. Interest is charged only on the funds released at each stage, not on the full loan amount, which reduces total financing costs during the build period. Lenders require progress draw inspections confirming each milestone before releasing the next fund tranche. Construction mortgage rates typically run 0.50% to 1.25% above standard residential rates. Once the home is complete and passes final inspection the construction mortgage converts to a standard residential mortgage at current term rates. The shorter four to eight month prefab construction timeline meaningfully reduces total construction loan interest costs compared to traditional home construction which typically carries construction financing for twelve to eighteen months.

How can I qualify for a loan to build a prefab house in Ontario?

Qualifying for a construction loan to build a prefab house in Ontario requires meeting criteria across four distinct areas simultaneously. Borrower qualification includes a minimum credit score of 640 to 680 for major lenders, stable documented income, and gross and total debt service ratios within standard lender thresholds — all tested under the OSFI mortgage stress test at the greater of your contract rate plus 2% or the current qualifying rate. Property qualification requires owned land with registered title, zoning confirmation that residential construction is permitted, and a building site assessed as suitable for the chosen foundation type. Builder qualification requires CSA A277 certification from your manufacturer, a licensed engineer-stamped floor plan and engineering drawings, and a complete construction timeline with milestone dates. Documentation qualification requires all builder and property documents in lender-ready format before submission — incomplete documentation is the most common cause of delayed approvals on prefab construction mortgage applications. My Own Cottage provides the complete builder documentation package for every Ontario build in lender-ready format as a standard component of every project.

Do prefab homes qualify for CMHC insurance in Ontario?

Yes — CSA A277 certified prefab homes permanently affixed to a permanent foundation on owned land and used as the buyer’s owner-occupied primary residence qualify for Canada Mortgage and Housing Corporation mortgage insurance. CMHC insurance allows eligible buyers to purchase with as little as 5% down — the same minimum that applies to conventional site-built home purchases. Insurance premiums range from 2.80% to 4.00% of the insured loan amount depending on down payment percentage and can be added to the mortgage rather than paid upfront. Manufactured homes on leased land such as mobile home parks do not qualify for CMHC insurance. Confirming CSA A277 certification and permanent foundation details with your builder before approaching any lender accelerates CMHC eligibility confirmation significantly and prevents the most common documentation gap that delays prefab mortgage approvals.

What is the minimum down payment for a prefab home in Ontario?

The minimum down payment for a CSA A277 certified prefab home on owned land with CMHC insurance is 5% of the purchase price for properties under $500,000 — the same minimum that applies to conventional site-built home purchases. For purchases between $500,000 and $999,999 the minimum is 5% on the first $500,000 and 10% on the remainder. For purchases of $1,000,000 or more CMHC insurance is not available and a minimum 20% down payment is required for uninsured mortgages. Buyers who already own land can sometimes use the assessed land value as equity toward their down payment requirements — confirm this approach with your specific lender before finalizing your financing structure as acceptance policies vary across lenders.

What is the difference between a chattel mortgage and a traditional mortgage for prefab homes?

A traditional mortgage applies to prefab homes permanently affixed to owned land — the land secures the loan, the home is classified as real property, standard amortization and rate structures apply, and CMHC insurance is available. A chattel mortgage applies to prefab homes on leased land such as mobile home parks — the home itself is the collateral rather than land, the home is classified as personal property similar to an auto loan, amortization is shorter typically 15 to 20 years, interest rates are higher, and CMHC insurance does not apply. The distinction is the difference between homeownership as real estate and homeownership as personal property — with meaningfully different financing costs, loan terms, and long-term value trajectories. Wherever possible Ontario prefab home buyers should purchase on owned land to access the full range of residential financing options at standard rates.

What credit score do I need to finance a prefab home in Ontario?

Most major banks and non-bank lenders require a minimum credit score of 640 to 680 for standard prefab construction mortgage approval in Ontario. Credit unions may accept lower scores with compensating factors such as larger down payments or strong income documentation. Alternative lenders offer approval for buyers with credit scores below 640 at higher interest rates. Private lenders offer the most flexible credit history requirements at the highest rates — typically used as a short-term bridge solution while credit is being rebuilt before refinancing with a standard lender after construction completion. Regardless of credit score all borrowers must pass the OSFI mortgage stress test which determines the maximum loan amount available at any given income level.

Are there government programs supporting prefab home financing in Ontario?

Yes — four significant programs reduce the cost of prefab home ownership for qualifying Ontario buyers and each operates differently from the others. The Ontario new home HST rebate returns a portion of the provincial 8% HST component on qualifying new home purchases used as primary residences — representing $8,000 to $15,000 on projects in the $200,000 to $350,000 range. The federal GST relief program removes the 5% federal component on qualifying new home purchases up to $1.5 million for eligible first-time homebuyer households — representing approximately $10,000 to $15,000 on qualifying projects. The CMHC Green Home program offers mortgage insurance premium refunds of 15% to 25% for buyers who build to energy-efficient standards — prefab homes built to Passive House or net zero specifications frequently qualify. Canada Greener Homes grants of up to $5,000 are available for qualifying energy efficiency upgrades on new and existing homes including high-performance prefab builds. Confirm eligibility for all four programs with your accountant and builder before signing any purchase agreement — the combined effect can represent a five-figure reduction in total project cost.

How do financing terms for prefab homes differ from traditional homes in Ontario?

The financing terms for a CSA A277 certified prefab home on owned land are equivalent to a site-built home once the home is built and permanently installed — same lenders, same rates, same amortization periods, same CMHC insurance eligibility. The differences apply only during the construction phase and depend on the financing structure used. Construction mortgages carry rates 0.50% to 1.25% above standard residential rates and release funds in staged draws rather than as a lump sum. The construction interest period for a prefab build is four to eight months versus twelve to eighteen months for site-built construction — producing a meaningful total financing cost advantage for prefab buyers at current interest rates. Chattel mortgages for homes on leased land carry meaningfully different terms from traditional mortgages — shorter amortization, higher rates, and no CMHC eligibility — but these terms do not apply to permanently affixed prefab homes on owned land which are treated identically to site-built homes by all major lenders.

Can I get a self-build loan for a prefab home in Ontario?

Yes — owner-builder and self-build financing structures are available for Ontario prefab home buyers who want to arrange their own trades for finishing work rather than purchasing a fully delivered-and-installed package. A self-build construction mortgage follows the same staged draw structure as a standard prefab construction mortgage — funds release at verified build milestones — but lenders apply additional scrutiny to owner-builder applications because the borrower is also acting as the general contractor. Most major banks require owner-builders to demonstrate construction management experience or to retain a licensed contractor for at least the structural and mechanical phases of the build. CSA A277 certification from the prefab manufacturer is still required regardless of who manages the site work. Credit unions and alternative lenders are generally more flexible on owner-builder applications than major banks. The builder’s shell or kit home tier of prefab construction — where the buyer purchases the structural package and arranges all finishing — is the most common structure for self-build prefab projects in Ontario.

Which banks finance prefab homes in Ontario?

All major Canadian banks — RBC, TD, Scotiabank, BMO, and CIBC — offer construction mortgages and standard residential mortgages for CSA A277 certified prefab homes on owned land meeting Ontario Building Code requirements. Non-bank mortgage lenders including THINK Financial and First National offer competitive rates and more flexible approval criteria for factory-built homes. Credit unions including Meridian, Alterna, and DUCA provide prefab-friendly financing with more flexible underwriting — particularly for rural Ontario builds where local appraisers understand regional market nuances. Alternative lenders including Home Trust and EQ Bank offer approval for buyers who do not meet standard bank qualification criteria. The key to working with any of these financial institutions is having complete CSA certification and builder documentation in lender-ready format before making any application — this single factor more than any other determines approval timelines for prefab home financing across all lender types.

Does the Ontario HST rebate apply to prefab homes?

Yes — the Ontario new home HST rebate applies to qualifying new prefab home purchases used as primary residences on owned land when the structure is permanently affixed to a foundation. The rebate returns a portion of the provincial 8% HST component — representing $8,000 to $15,000 on projects in the $200,000 to $350,000 total cost range. The federal GST relief program removes the 5% federal component on qualifying new home purchases up to $1.5 million for eligible first-time homebuyer households — representing approximately $10,000 to $15,000 on projects in the $200,000 to $300,000 range. Combined these programs can represent a five-figure reduction in total project cost — reducing both the loan amount required and the CMHC insurance premium calculated on that amount. Confirm eligibility and structure the purchase correctly with your accountant before signing any purchase agreement to ensure the rebate applies to your specific transaction structure.

Can I use a HELOC to finance a garden suite or ADU in Ontario?

Yes — home equity loans and Home Equity Lines of Credit are among the most common and cost-effective financing solutions for garden suite, laneway home, and accessory dwelling unit builds on existing Ontario residential properties. The existing property secures the line of credit eliminating the need for a new construction mortgage and the associated draw inspection fees and administrative timeline. Funds are drawn as needed during the build providing flexible cash flow management during site preparation, foundation, and installation phases. HELOC financing is particularly well-suited to garden suite builds because the rental income generated by the completed secondary dwelling can service the debt independently of the primary household income. A garden suite generating $1,800 to $2,500 per month in rental income on a typical HELOC balance effectively becomes self-financing over a four to eight year period. Ontario’s Bill 23 provisions have reduced or eliminated development charges for qualifying ADU builds in many municipalities making the total project cost lower and the rental income to debt service ratio more favourable than at any previous point in Ontario’s housing market.

How long does it take to get financing approval for a prefab home in Ontario?

Construction mortgage approval for a prefab home in Ontario typically takes two to four weeks from complete documentation submission to approval confirmation — assuming CSA certification records, engineering drawings, construction timeline, cost breakdown, and borrower qualification documentation are all submitted simultaneously in lender-ready format. Incomplete documentation is the primary cause of delayed approvals and can extend the financing process by four to eight additional weeks as lenders request missing items sequentially. Standard residential mortgage approval for an already-built prefab home on owned land follows the same two to four week timeline as a standard residential purchase mortgage. Working with a lender or mortgage broker experienced in factory-built home financing and having complete builder documentation in lender-ready format before making any application are the two most effective strategies for minimizing approval timelines across all lender types.

What documentation does my builder need to provide for prefab home financing?

Lenders require eight specific documentation items from your prefab home builder for construction mortgage approval in Ontario. CSA A277 certification records confirming the factory construction process meets Canadian Standards Association standards. Engineering drawings and floor plan specifications stamped by a licensed engineer. A detailed construction cost breakdown covering all line items from foundation through occupancy. A construction timeline with milestone dates aligned with the proposed draw schedule. A site plan showing permanent foundation location, setbacks, and utility access. Builder credentials and track record documentation including previous project completions. Evidence of home warranty enrollment through Tarion for the specific project. Land ownership documentation and zoning confirmation for the building site. My Own Cottage provides all eight items in lender-ready format as a standard component of every Ontario build — eliminating the documentation gap that most commonly delays prefab construction mortgage approvals.

What is the typical construction mortgage interest cost saving on a prefab build versus traditional home construction?

The construction loan interest cost saving from a prefab build’s shorter timeline is one of the most significant and least discussed financial advantages of factory-built home construction in Ontario. On a $400,000 construction loan at 7% annual interest the difference between a four-month prefab timeline and an eighteen-month site-built construction timeline is approximately $23,000 in construction loan financing costs before the mortgage converts to a standard term. This saving compounds at higher loan amounts and in higher interest rate environments — making it an increasingly important factor in the prefab versus site-built total cost comparison as Ontario construction costs and interest rates remain elevated. A buyer comparing prefab versus traditional home construction costs who omits the construction loan interest differential is underestimating the true cost advantage of prefab by a significant margin.

Ready to Finance Your Ontario Prefab Home?

Understanding the complete financing picture before selecting a model is what makes the difference between a prefab home project that proceeds smoothly from consultation to occupancy and one that stalls at the financing stage after model selection.

My Own Cottage provides complete all-in cost estimates and lender-ready documentation for every Ontario build before you commit to anything.

No surprises. No hidden costs. No pressure.

Just honest numbers specific to your land, your model, and your timeline — backed by Ontario’s new home warranty through Tarion and built to CSA A277 certified factory standards that qualify for standard mortgage financing and CMHC insurance.

Book a free consultation with My Own Cottage — we will walk you through realistic total project costs, the right financing structure for your specific build situation, and the complete lender documentation package that accelerates your approval.

🧑💼 Request a Free Consultation

📲 Call Us Directly: (705) 345-9337

🏘️ View Our Design Catalogue

✅ Ontario-Built | ⚡ Energy-Efficient | 🏡 Fully Customizable | 🚚 Fast Delivery

Alternatively, for your convenience, you can also simply fill out the contact form below and we’ll get back to you soon! 👇

Contact Us

We usually respond within 24 hours!

- Comprehensive Warranty

- Best Price Guarantee

- Exceptional Service

Verified External Resources

Ontario Building Code — Official provincial regulations governing modular and factory-built homes in Ontario.

CSA A277 — Canadian Standards Association certification standard for factory construction processes.

Tarion Warranty Corporation — Ontario’s new home warranty provider covering registered builder enrollment and warranty coverage.

CMHC — Canada Mortgage and Housing Corporation — Federal housing authority covering modular and prefab home financing eligibility and CMHC insurance.

CRA — HST Rebate and GST Relief Programs — Federal and provincial tax relief programs for qualifying new home purchases.